Sri Lanka’s primary dealers are excessively utilizing the Central Bank’s standing facilities to finance their government securities portfolios, despite being excluded from liquidity auctions, according to a recent International Monetary Fund (IMF) report.

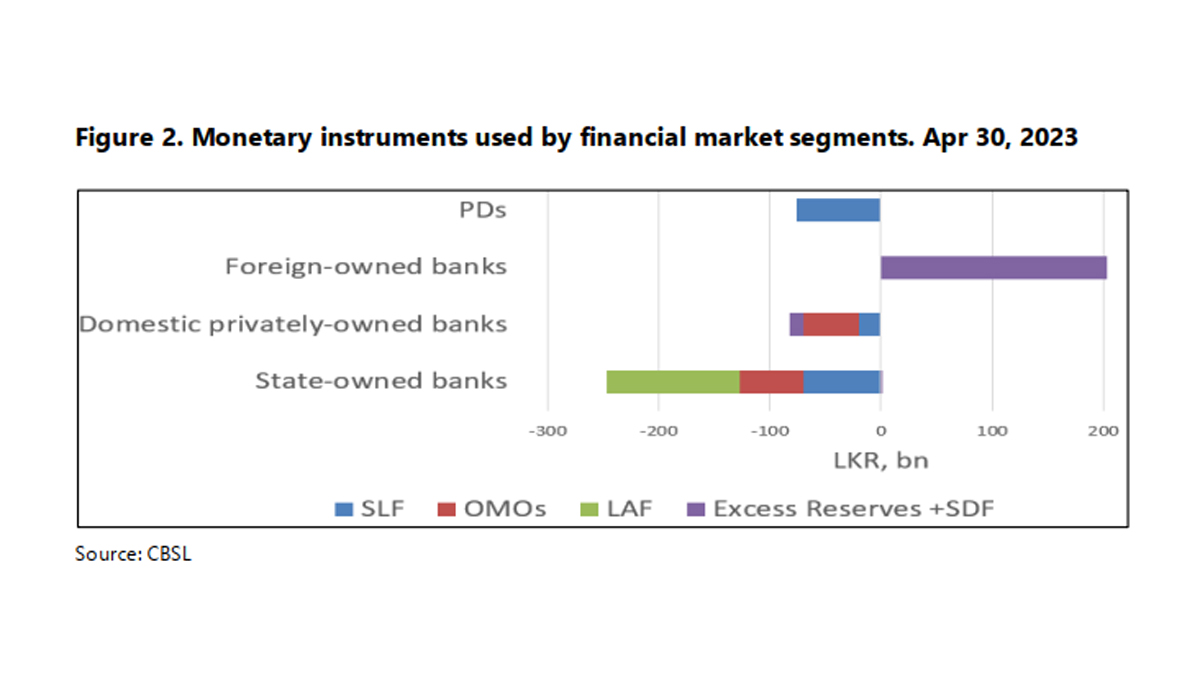

The report highlights that non-bank primary dealers for government LKR debt have access to the Central Bank’s Standing Lending Facility (SLF) and frequently use it to finance their portfolios. As of the end of April 2023, non-bank primary dealers accounted for approximately 46% of SLF usage, amounting to around LKR 76 billion.

The IMF recommends that the Central Bank of Sri Lanka begin phasing out the use of monetary instruments to support the development of the LKR bond market. The report stresses that monetary policy tools should not be extended to non-bank primary dealers to support their activities in the LKR bond market.

Currently, primary dealers are already barred from open market operation auctions. However, in countries with low inflation and floating exchange rates, such as the United States, central banks provide liquidity facilities to dealers. Analysts note that the use of central bank standing facilities should only be for clearing transactions on a single day and not for prolonged periods. Ideally, any borrowings should be cleared by selling securities to real investors before the next auction.

In Sri Lanka, due to the unique way Treasury bills are sold—where dealers are often forced to purchase them at later stages after initial auctions—dealers frequently lack the funds to pay for them. This has exacerbated their reliance on the Central Bank’s standing facilities.

In reserve-collecting central banks, the question of whether inflationary open market operations provide liquidity to banks, non-bank primary dealers, or even the government directly is irrelevant. The balance of payments would still go into deficit, and the government would face difficulties repaying maturing debt, regardless of which counterpart receives liquidity injections.

Moreover, if private credit is refinanced through open market operations, imports could surge faster than when government spending is financed, as most government expenses are domestic. Banks that receive central bank credit can lend to customers without adequate deposits, triggering an external imbalance, currency depreciation, and heightened demand for foreign currency, further contributing to domestic credit spikes and liquidity injections.

Historically, state-owned banks have been the most significant users of such facilities, while foreign banks tend to maintain excess reserves. If Sri Lanka did not have a policy rate, or had a narrowly targeted call rate, excess reserves would lead to an automatic rise in foreign reserves, similar to the period before the establishment of the Central Bank in 1950. At that time, government deposits with the monetary authority also boosted foreign reserves.

However, when a soft-pegged central bank—one that creates chronic forex shortages and depreciation due to a flawed operational framework—injects money under the assumption of a “structural shortage,” it results in a permanent loss of foreign reserves. This situation occurs typically after forex market interventions.

Money obtained by banks from selling Treasury bills to the Central Bank may also be used to refinance domestic credit, leading to further currency depreciation and reserve depletion. Allowing primary dealers to participate in auctions could, however, help the Central Bank quickly respond to market conditions, raising the refinancing rate to a ceiling and avoiding balance of payments deficits.

In reserve-collecting central banks, high bid rates from primary dealers can signal the need for the Central Bank to increase the ceiling policy rate to protect foreign reserves.

Balance of payments issues began to surface in Western nations after the Federal Reserve introduced the policy rate and open market operations in the 1990s. Meanwhile, countries like Singapore, Hong Kong, Cambodia, and the GCC nations have avoided currency depreciation, banking crises, and political instability by refraining from adopting a policy rate.

{kind=link}