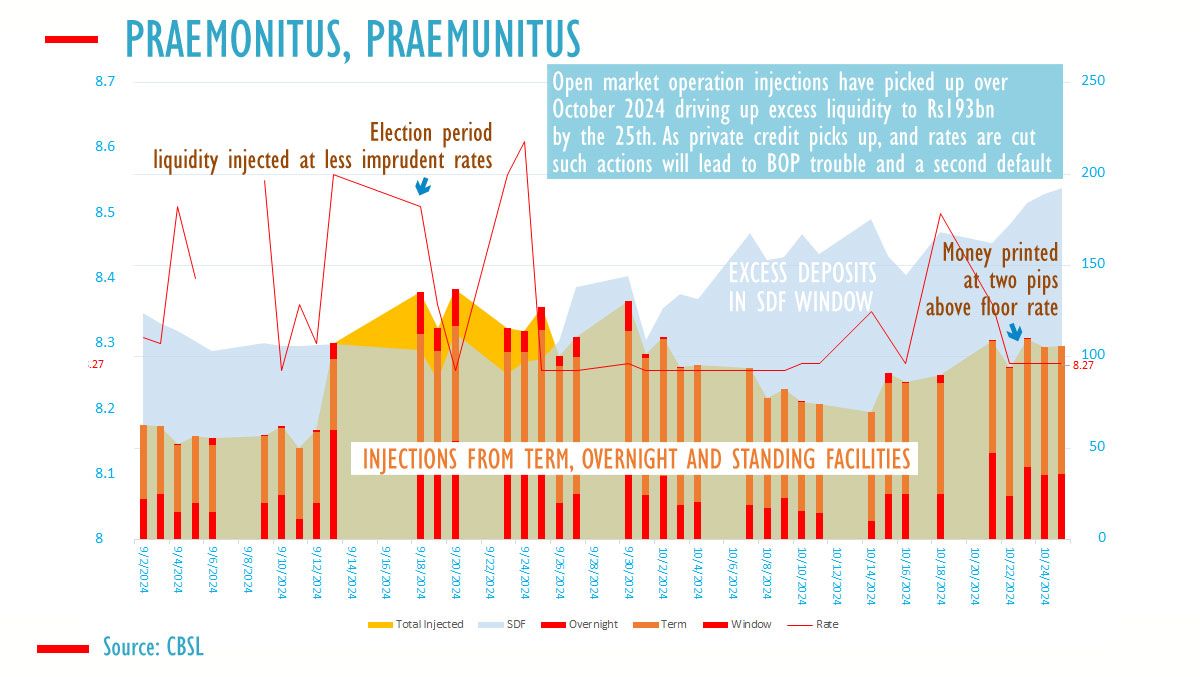

By October 25, Sri Lanka’s central bank injected approximately 100 billion rupees into the financial system through various liquidity mechanisms, significantly increasing surplus money in the banking sector to over 190 billion rupees, official data reveals. Specifically, 36.16 billion rupees were infused through an overnight auction, and another 70 billion rupees were injected for a seven-day term through money printing.

Excess liquidity held in the central bank’s standing facility rose to 193.4 billion rupees, marking a steep increase from 138 billion rupees just a month prior.

Interest Rate at 8.27 Percent

At an interest rate as low as 8.27 percent—only marginally above the policy floor rate—the central bank offered 40 billion rupees, of which only 36 billion rupees were bid. This action minimized the need for market participants to borrow at the 9.25 percent standing facility rate, enabling more market activity without immediate deposits. However, with upcoming elections and possible cash drawdowns, some banks utilized the standing facility, borrowing at 9.25 percent.

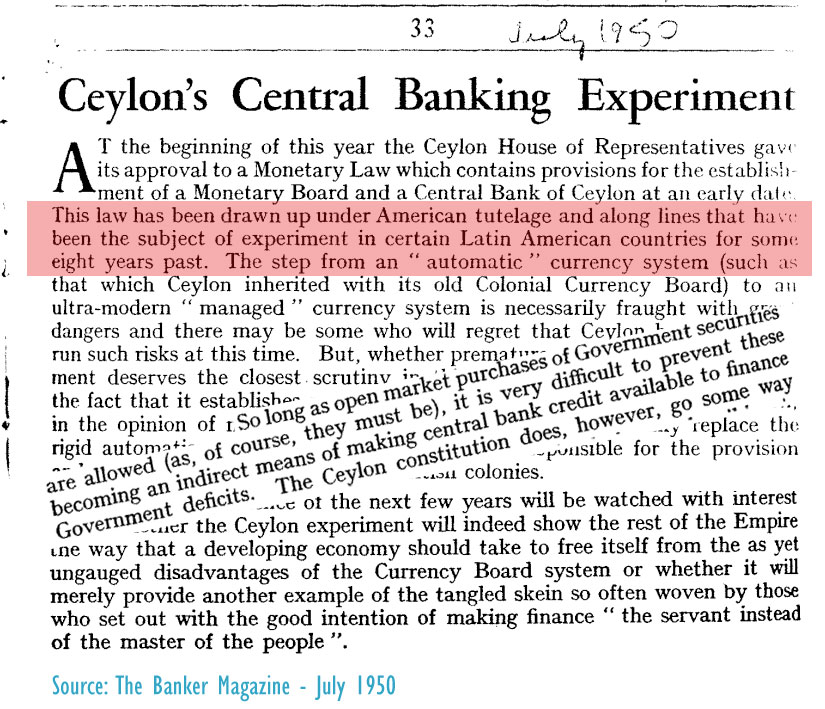

Since its inception in 1950, the central bank has employed a range of measures to influence rates, occasionally leading to currency shortages, financial instability, and associated socioeconomic impacts, including food insecurity and social unrest. Historically, such policies spurred trade restrictions and high interest rates, mirroring similar trends seen globally until shifts in monetary policies, such as those introduced by Paul Volcker in the 1980s.

A Contested ‘No Money Printing’ Policy

Despite claims that new discretionary monetary laws prevent unchecked money printing, the central bank retains considerable power to inject liquidity into the financial system through open market operations. With a 5 percent inflation target set by former President Wickremesinghe, the central bank gained greater policy autonomy—a move that has been questioned in light of expectations for a stable exchange rate.

IMF’s recent reports highlight concerns regarding central bank funding practices, particularly its role in supporting commercial banks rather than focusing solely on primary dealers, who typically receive short-term funding.

Suppressing Gilt Yields?

While the rationale behind the large-scale liquidity injections remains unclear, some analysts suggest it may serve to lower government bond yields, indirectly supporting deficit financing. Notably, Sri Lanka’s original central bank framework, established by John Exter, did not endorse direct bond purchases at auction, emphasizing instead the risks of encouraging imports in an export-dependent economy.

However, with a flexible exchange rate and reduced regulatory constraints since 1978, some analysts argue that inflationary pressures have intensified, prompting periodic interventions by the IMF.

Modern politicians often lack a deep understanding of state-owned central banks’ domestic operations, a knowledge base more common among 19th-century lawmakers. Back then, legislators introduced effective policies to limit the Bank of England’s discretionary powers, creating a solid legal anchor to curb inflation and currency crises.

Today, rate cuts through Open Market Operations (OMO) can destabilize exchange rates and drive speculative behavior among exporters and importers, eventually leading to capital flight, loss of confidence, and higher interest rates—a pattern seen since 2015.

Instrument Independence and Its Consequences

Sri Lanka’s recent 5% inflation target, ratified under former President Ranil Wickremsinghe’s administration via a new monetary law, grants the central bank extensive autonomy. This independence may facilitate the misuse of financial instruments, triggering external pressures and elevating nominal interest rates during stabilization crises. In contrast, when Sri Lanka’s central bank was established in 1950, Treasury bill yields were below 1%, and concepts like “real” interest rates were almost unknown. As central banks increasingly targeted short-term rates, inflation surged, and “real” interest rates became essential in economic analysis, even though many inflation-era economists were more versed in statistics than monetary operations.

“There wasn’t a focus on real interest rates then because inflation wasn’t expected,” Paul Volcker remarked in a 2008 interview, reflecting on his years with the U.S. Treasury and the Federal Reserve.

Through OMOs, the Federal Reserve fueled an economic bubble and the Great Depression without any war—a pattern that resurfaced after the IMF’s 1978 Second Amendment, despite low deficits and high revenue-to-GDP ratios in Latin American economies.

The Impact of a Single Policy Rate and Historical Context

The idea of a single policy rate with fixed-rate injections originated with Scottish Mercantilist John Law, but was initially resisted by classical economists until adopted by the Fed. This setup ultimately led to decentralized money printing and the establishment of an open market committee, which ironically produced opposite outcomes. Mexico’s 1994 debt crisis is one example, where OMOs led to instability amid a budget surplus and strong private credit.

Through OMOs, the “independent” Federal Reserve dismantled Bretton Woods, ignited the Great Inflation, and set off the housing bubble.

Muted Economy and Post-War Fed Actions

In times of weak private credit, central banks may print money with limited immediate instability. During World War II, the Federal Reserve purchased multiple-maturity Treasuries to keep rates down, with fewer Balance of Payments (BOP) issues than those following the war’s end in 1951 and during the 1960s and 1970s. However, once private credit surged, the Fed halted these activities to avoid worsening shortages and rationing, which officially ended in the U.S. in 1947. Later, efforts to defend Liberty Bond prices led to what’s known as the Korean War bubble, while the Fed-Treasury Accord marked the beginning of an “independent” Fed, shifting focus away from long-term bond purchases.

Despite early leadership under Marriner Eccles, a banker with deep knowledge of central banking, this understanding faded within a decade, and the Fed introduced central bank swaps to mitigate inflation and balance-of-payments issues stemming from rate cuts aimed at “full employment.”

IMF Programs and Economic Reform Myths

IMF intervention surged in the 1960s, with Sri Lanka beginning its IMF programs mid-decade. Programs were initially short-term, aimed solely at addressing BOP issues, not economic reform. Reform-focused programs emerged later, inspired by Margaret Thatcher’s success, although replication efforts, especially in Latin America, often failed. Competitive exchange rate policies heightened social unrest and led to further defaults, as budgets became unmanageable. Thatcher’s reforms, notably conducted outside the UK’s final IMF program, were among the few that met with sustainable success.

{kind=link}