KEY DEVELOPMENTS

Sri Lanka is expected to reach board level agreement for an Extended Fund Facility (EFF) with the IMF on 20th March 2023, exactly 200 days after reaching staff level agreement. The EFF will provide 2.9 billion USD in foreign currency reserves support for a period of about four years. It is not budget support; so, it cannot be used for government expenditure, as often assumed in media reporting.

Despite suspending international debt repayment, Sri Lanka’s total debt continues to increase as payments that are due, accrue as arrears and local currency debt to finance government expenditure increases. By December of 2022, the total outstanding public debt had increased to USD 84 billion (128% of GDP), an increase from USD 80 billion (121% of GDP) as of June 2022. Sri Lanka suffered severe currency volatility with a sudden depreciation in March 2022, and the currency volatility was adversely impacted by the sudden appreciation of the currency in March 2023

The IMF Facility for Sri Lanka and the path ahead

With the assurances from India, China, the Paris Club, and private bondholders to support the IMF pro[1]gram, and provided the government’s commitments to the targets and reforms specified in the program are accepted by the IMF board, Sri Lanka will meet the criteria for achieving a board-level agreement for the IMF program. As the staff-level agreement for Sri Lanka on the 1st of September 2022 states:

“Debt relief from Sri Lanka’s creditors and additional financing from multilateral partners will be required to help ensure debt sustainability and close financing gaps. Financing assurances to restore debt sustainability from Sri Lanka’s official creditors and making a good faith effort to reach a collaborative agreement with private creditors are crucial before the IMF can provide financial support to Sri Lanka.”

The expected IMF board-level agreement is for an Extended Fund Facility (EFF) for Sri Lanka. It has raised hopes of an immediate economic turnaround. The program, however, is only a necessary early step on a long road to economic recovery. The task of recovering debt sustainability is still ahead, resting on the government’s ability to reduce its deficit and renegotiate its debt terms with lenders, regain its ratings, and access to international financial markets. Prospects of a sustainable recovery rest on the government’s execution of these commitments, and ability to recover local and global confidence.

Sri Lanka’s EFF is for Reserve Support not Budget Support

The statements of the IMF indicate that the funds from the EFF will support the immediate reserve position, and the future balance of payment position only, and not the country’s capacity to meet its budgetary costs. As the staff-level agreement states: “The objectives of Sri Lanka’s new Fund-supported program are to restore macroeconomic stability and debt sustainability, while safeguarding financial stability, protecting the vulnerable, and stepping up structural reforms to address corruption vulnerabilities and unlock Sri Lanka’s growth potential.”

The uses of the funds are given explicitly as those that “restore macroeconomic stability and debt sustainability”. This should be considered in the context of the overall objective of the EFF lending facility of the IMF, which is to: “provide assistance to countries experiencing serious payment imbalances because of structural impediments or slow growth and an inherently weak balance-of-payments position.” This above statement on Sri Lanka contrasts

with the 30-month EFF agreed with Argentina on the 25th of March 2022, which states: “The authorities’ IMF-supported program provides Argentina with balance of payments and budget support that is tied to specific measures to strengthen public finances, tackle persistent high inflation, boost reserve accumulation, and set the basis for more sustainable and inclusive economic growth.” Comparing these statements, the program for Sri Lanka does not offer “budget support”, unlike in the case of Argentina.

The EFF for Sri Lanka is likely to be restricted for use by the Central Bank as additional reserves, which might help relax some of the tight import and capital outflow restrictions currently in place. However, these funds would not be usable as budgetary support to the government and hence would not reduce the government’s borrowing needs.

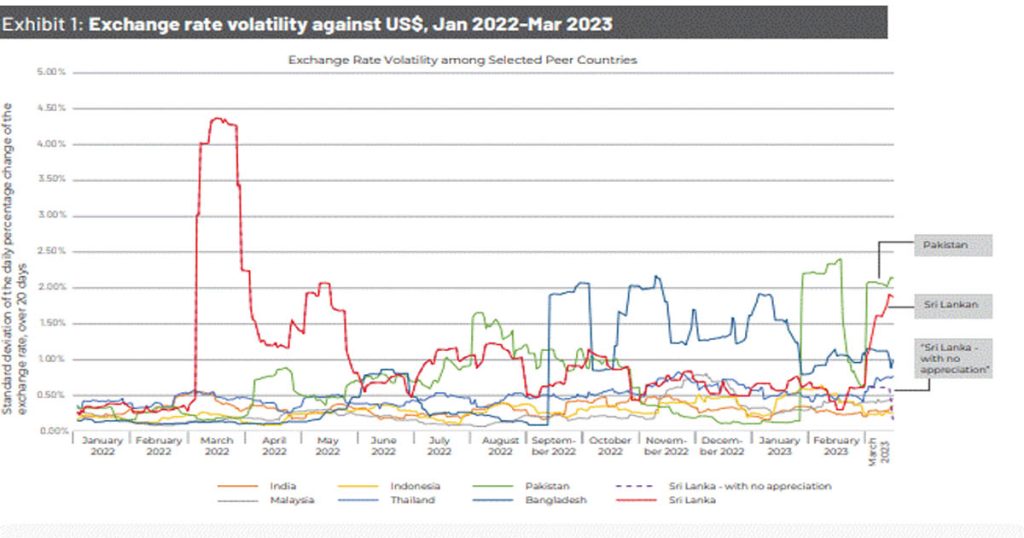

Volatility versus appreciation – missing the point in exchange rate management

The movement of the Sri Lankan Rupee (LKR) against the United States Dollar (USD) has been the focus of media and public attention since the onset of the economic crisis. In recent weeks the LKR appreciation against the USD was seen as a sign of recovering economic stability. However, Verité Research analysis shows that the more critical factor for economic stability and businesses confidence is exchange rate volatility rather than the rate or its appreciation.

From January 2023 to the 16th of March 2023 the LKR has appreciated against the USD – reducing by 7% the LKR required to purchase 1 USD. Exhibit 1 compares the volatility of LKR exchange rate — measured as the standard deviation of the daily percentage change over 20 days — to other currencies in the South and South Asian region, including the Indian Rupee, Indonesian Rupiah, Malaysian Ringgit, Thai Baht, Pakistani Rupee, and the Bangladeshi Taka.

Verité Research analysis in Exhibit 1 demonstrates that, from January to March 2023, the LKR exhibited significant volatility compared to other currencies in the sample, with only Pakistan’s currency displaying greater volatility in March 2023. Currently, the described volatility measure stands at 1.88%. Although the LKR appreciated against the USD to LKR337/USD as of 16th of March 2023, the volatility of the LKR would have improved to 0.15% had the currency not appreciated and remained at LKR362/USD.

The increase in volatility of the LKR coincides with the relaxing of capital flow constraints. A greater volatility in exchange rates increases uncertainty and risk for businesses as well as investment. Therefore, it can be more important for Sri Lanka to focus on minimizing the volatility of the exchange rate, rather than maximizing its appreciation. This will help reduce uncertainty and risk premiums that hamper growth in economic activity.

Source : The Verité Research Debt Update